The Lending and Asset-Based Financing Lifecycle: A Guide for Early-Stage Fintechs

A step-by-step guide to building a scalable, investor-ready lending infrastructure

Introduction

Building a lending business is rewarding, but also complex. For early-stage fintechs and asset originators, the journey from issuing your first loans to accessing institutional debt can feel overwhelming, full of acronyms, processes, and investor requirements. Terms like borrowing base, covenants, or waterfalls may sound distant from the daily work of acquiring customers and funding loans, yet they are the foundations of sustainable growth.

The purpose of this article is to provide a clear roadmap for that journey. We’ll walk through the full lifecycle of a scalable lending business: starting with the basic lending workflows that form the operational foundation, moving into the asset-based financing processes that open the door to institutional debt, and finally exploring the advanced capabilities that strengthen forecasting and control. At each stage, we’ll highlight key processes, common pitfalls for early-stage fintechs, and how Fence supports you in building for scale. The entire lifecycle is also summarized in two graphs below, which you can use as a visual guide while reading.

Too often, originators delay building this infrastructure, relying on spreadsheets and manual checks. But once scale and external capital come into play, these stop being temporary fixes and become real bottlenecks. In many cases, teams also invest their own engineering resources into building systems that quickly become outdated or are deprioritized because they aren’t the company’s core business focus. The result is sinking valuable time into cumbersome, non-value-add operations. Lenders, meanwhile, expect transparency, real-time visibility, and robust controls. Without them, fintechs risk credibility and, ultimately, access to capital.

We hope the workflows outlined here serve as practical guidelines to help fintechs and asset originators build stronger foundations and scale their lending business with confidence.

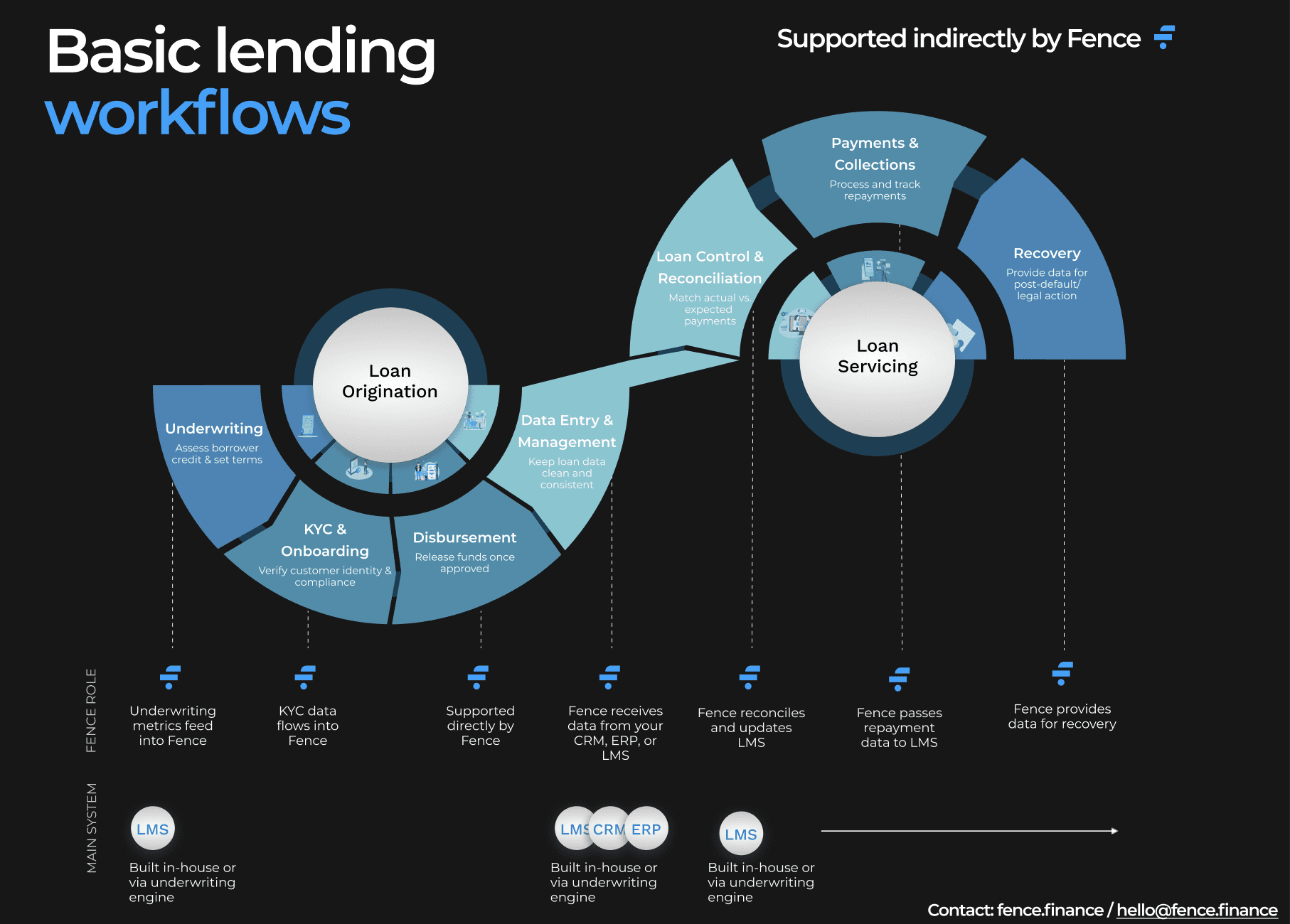

Part 1 – Basic Lending Workflows

Without these, you don’t have a lending business.

Every lending company rests on a few essential workflows. They may seem routine, but they are the foundation on which everything else is built. At this stage, the focus is on two main areas: loan origination, where credit is evaluated, customers are onboarded, and funds are disbursed; and loan servicing, which ensures repayments are tracked, reconciled, and recovered when necessary. If these processes are incomplete or inconsistent, scaling, and especially attracting institutional capital, becomes extremely difficult.

1. Loan Origination

The goal of this stage is to establish the workflows that allow a fintech lender to originate loans in a structured, scalable, and compliant way. Each step has functional blocks that must be covered end-to-end, with critical build vs. buy decisions.

Funding

Description: Funding is the first building block of any lending business, as it provides the initial capital to issue loans. Early-stage fintechs typically start with FFF (friends, family, founders) or early equity rounds, and in some cases partner with established lenders who provide the capital and tech lending infrastructure while the fintech retains an origination fee. These structures give originators a way to test their models and prove demand without tying up their own balance sheet.

Key decisions: Important considerations at this stage include retaining access to track-record data, the level of technology dependency on external providers, control over pricing and loan terms, and the speed with which funding can be deployed to customers.

Systems involved: Some examples of embedded finance platforms include Defacto or SeQura in Europe and OatFi or Parafin in the US.

Underwriting

Description: Underwriting defines who is eligible for credit, how much they can borrow, and at what price. This involves combining rules-based decisioning, scorecards, machine learning models, and credit policies to manage risk while supporting growth.

Key decisions: Early-stage lenders must weigh important choices such as whether to build models in-house or rely on third-party engines, how much and what type of data to use, and the level of explainability required to meet regulatory expectations. For fintechs, the real competitive edge in a lending segment often comes from their ability to harness unique data and apply it in a differentiated way—making it critical to develop and iterate the underwriting algorithm from the outset. They also need to monitor for model drift as portfolios evolve and decide the right balance between automated approvals and manual reviews for borderline cases.

Systems involved: Usually, an internally built logic framework with both automated and escalation pathways. For sideline businesses, lenders may turn to an underwriting engine provider, or use an LMS with underwriting capabilities such as Alloy or Provenir.

KYC & Onboarding

Description: After defining underwriting rules and credit policies, lenders need to ensure that only verified, compliant borrowers enter the system. KYC and onboarding serve this purpose, covering lead capture, digital identity verification, sanctions and PEP screening, and ongoing AML monitoring.

Key decisions: Early-stage lenders must balance conversion rates against regulatory friction, adapt workflows to country-specific compliance requirements, select reliable providers for ID and AML checks, and securely store evidence for audit readiness.

Systems involved: KYC/AML providers such as Onfido or Trulioo can help demonstrate compliance.

Disbursement

Description: Once borrowers are onboarded and approved, the next challenge is to move money. Disbursement is the process of releasing funds accurately, securely, and on time, tying the credit decision to the actual customer experience. This requires seamless integration with payment rails and treasury systems, robust retry mechanisms for failed payouts, and alignment with eligibility and documentation checks.

Key decisions: Lenders need to select a payment provider that seamlessly integrates with their business flow, manages payout failures and exceptions (e.g., returns), and offers coverage across their target markets—all while remaining cost-efficient and scalable.

Systems involved: Stripe Treasury, GoCardless.

Data Management

Description: Behind every origination workflow—whether it’s KYC, underwriting, or disbursement—sits the data that powers decisions and reporting. Data management is about ingesting and normalizing information from banks, payroll systems, accounting platforms, credit bureaus, and open banking APIs.

Key decisions: Fintechs must decide between batch and real-time ingestion, implement monitoring to ensure data quality, and comply with privacy standards like GDPR. Clean, reliable data pipelines are critical for investor trust, operational efficiency, and long-term scalability. It’s not just about data accuracy but about having a data framework that helps you run a sound lending business (e.g., knowing the best action for each of your customers).

Systems involved: Often an internally built logic framework, an LMS, a CRM, or an ERP system.

2. Loan Servicing

Once loans are originated, the focus shifts to ensuring repayments are tracked, reconciled, and recovered when needed. Effective servicing not only protects cash flow but also builds the transparency and discipline that investors expect.

Loan Control & Reconciliation

Description: The first step in servicing is making sure that incoming repayments align with the payment schedule for each customer. This means reconciling borrower payments against records in the LMS, keeping balances accurate and portfolios clean, and having a clear next-best-action for each loan in the portfolio.

Key decisions: How frequently to run reconciliations (daily for near real-time oversight vs. monthly for smaller portfolios), the right balance between automation and manual checks, and how to resolve exceptions efficiently without slowing down reporting.

Systems involved: LMS.

Payments & Collections

Description: Once repayments start flowing, lenders need systems to capture them consistently and deal with inevitable failures. Collections processes include credit cards, automated debits, ACH, retry strategies, and promises-to-pay—all of which directly affect portfolio performance and customer relationships.

Key decisions: Which payment methods best fit the borrower base (ACH, SEPA, cards, wallets), how to handle failed transactions without creating friction, and whether to work with local processors for higher success rates or consolidate with global providers.

Systems involved: LMS with payment processors like Stripe, Adyen and GoCardless often integrated.

Recovery

Description: Even with strong origination and collections processes, some borrowers will go into delinquency and default. Recovery is about structuring how delinquent loans are managed—whether through internal teams, outsourced agencies, or legal action—while also capturing insights that improve future credit policies.

Key decisions: When to escalate from internal efforts to external partners, which borrower groups should be prioritized, and how jurisdiction-specific legal frameworks affect enforceability and recovery costs.

Systems involved: LMS. Specialized recovery tools like CollectAI or TrueAccord can also be connected.

How Fence can help in the basic lending workflows

Fence connects seamlessly to your existing tools to ingest data and acts as a second layer of control over your assets. This helps fintech teams cut down on manual reconciliations, gain real-time business performance insights (e.g., collection curves, NPL performance, covenant tracking), and free up bandwidth to focus on growth. At the same time, having an institutional-grade control layer also builds external credibility for investors when raising debt.

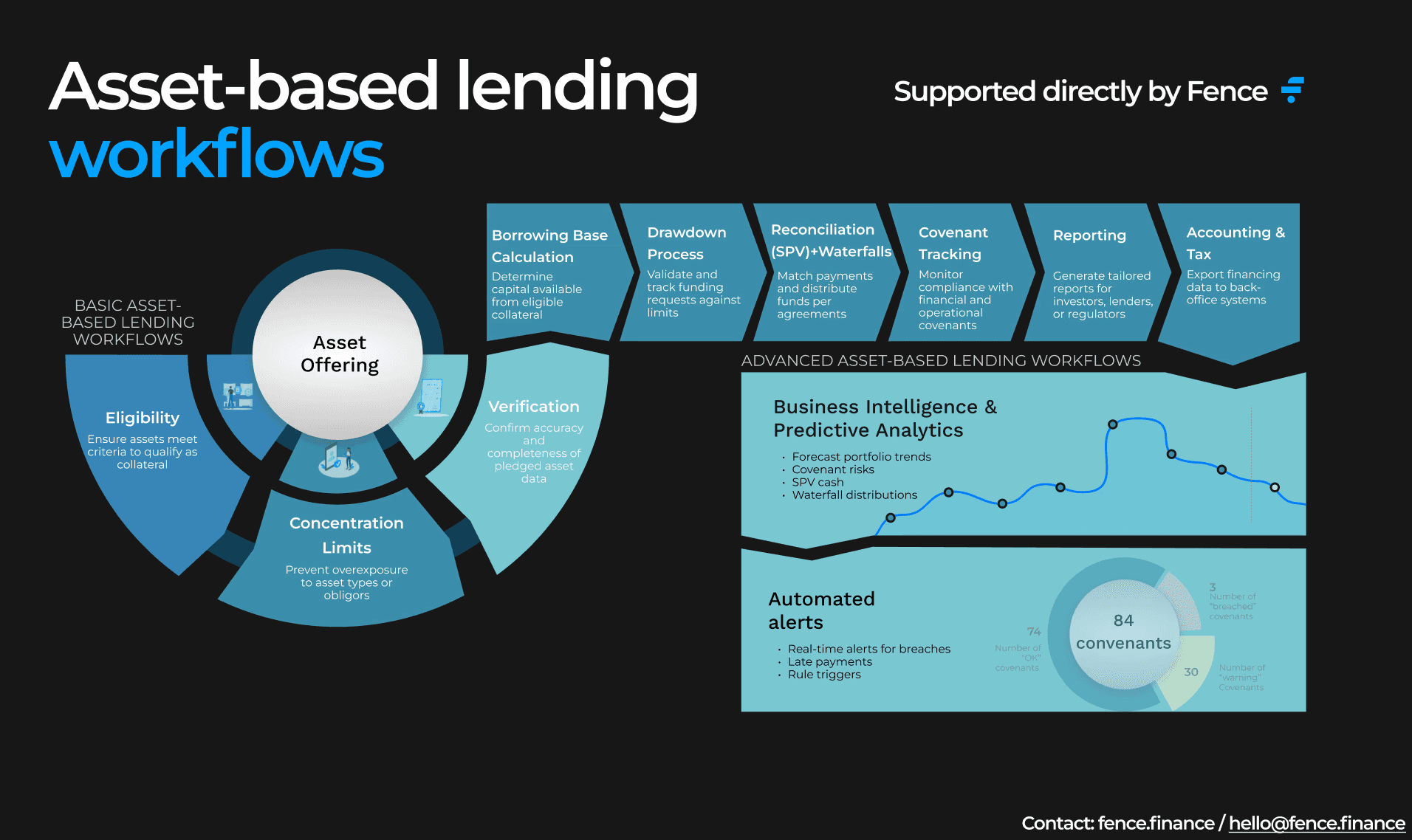

Part 2 – Basic Asset-Based Financing Workflows

Without these, you don’t have access to institutional debt.

Once you’ve established the fundamentals of loan origination and servicing, the next step is building the infrastructure that allows your loan book to be financed externally with an asset-based structure. This typically involves setting up a warehouse facility.

A warehouse facility is a financial structure that purchases a fintech’s assets at a given price, in return for the future cash flows of those assets. It’s used as a way to free up capital for fintechs, so they can keep growing without the need to use their equity.

This is where fintech lenders often feel the gap: investors require rigorous controls, standardized reporting, and transparent monitoring before they commit capital. The workflows below form the day-to-day foundation of any asset-backed financing structure.

1. Asset Offering

Capital providers require assurance that only eligible assets are included in the financing pool. This process involves verifying the existence of assets, applying eligibility criteria, enforcing concentration limits to maintain diversification, and validating the integrity of loan-level data. Fence connects to your data sources to perform all these controls, ensuring that collateral selection is both consistent and transparent.

2. Borrowing Base Calculation & Enforcement

Once assets have been screened and verified, the next step is determining how much financing capital providers will support. The borrowing base defines the amount of capital available against eligible collateral, and accuracy is critical as it underpins both lender confidence and liquidity management. Just as important as calculating the borrowing base is enforcing it—ensuring that originators never draw more than the collateral pledged to the facility. Fence automates both the calculation and the enforcement of these rules, applying them consistently across the portfolio and making borrowing capacity continuously visible.

3. Drawdown Process

Each funding request must align precisely with borrowing base availability and covenant restrictions. Manual processes often slow this step and increase risk for lenders. Fence validates and executes drawdowns through our platform. Put simply, fintechs come to our platform and ask for a drawdown, which arrives at their bank account in a matter of minutes. In a traditional process, a drawdown will typically take a week or more to process and are limited in frequency by investors. Fence eliminates that friction to allow access to Capital on Demand.

4. Reconciliation (SPV) + Waterfalls

Once funds have been drawn, collections from the assets flow through specific collection accounts, which are controlled and monitored by Fence. Fence calculates and distributes such cash according to pre-agreed priorities, often referred to as the waterfall. The platform also allocates collections to individual assets to keep track of asset performance in real time.

5. Covenant Tracking

The cash flows in warehouse facilities are typically subject to covenant compliance. Lenders want assurance not just that payments are made correctly, but that the portfolio continues to meet financial and operational requirements over time. The performance of such covenants is monitored continuously by Fence, turning operational data into real-time alerts that preserve transparency and confidence. This eliminates the burden from the fintech who can focus on tracking their own business.

6. Reporting

Covenant monitoring and reconciliation ultimately need to be communicated clearly to investors and stakeholders. Institutional debt depends on reliable reporting. They want timely, accurate, and tailored insights, not just raw data. By generating reports directly from structured information already captured in the workflows above, Fence ensures outputs are consistent, trustworthy, and available while reducing the time needed to produce these reports, again saving time and resources for the fintech.

7. Accounting & Tax

Finally, asset-based financing must integrate seamlessly with accounting and tax functions. While these processes are typically managed by dedicated systems, Fence provides structured exports, via API, CSV, or Excel, that keep financing data aligned with back-office requirements.

Part 3 – Advanced Asset-Based Lending Workflows

Turning compliance into foresight and control.

Once the foundational workflows are in place, the next stage is to enhance them with forward-looking tools. Advanced capabilities are not strictly required to launch a facility, but they increasingly distinguish originators that manage financing reactively from those that manage it strategically.

Business Intelligence & Predictive Analytics

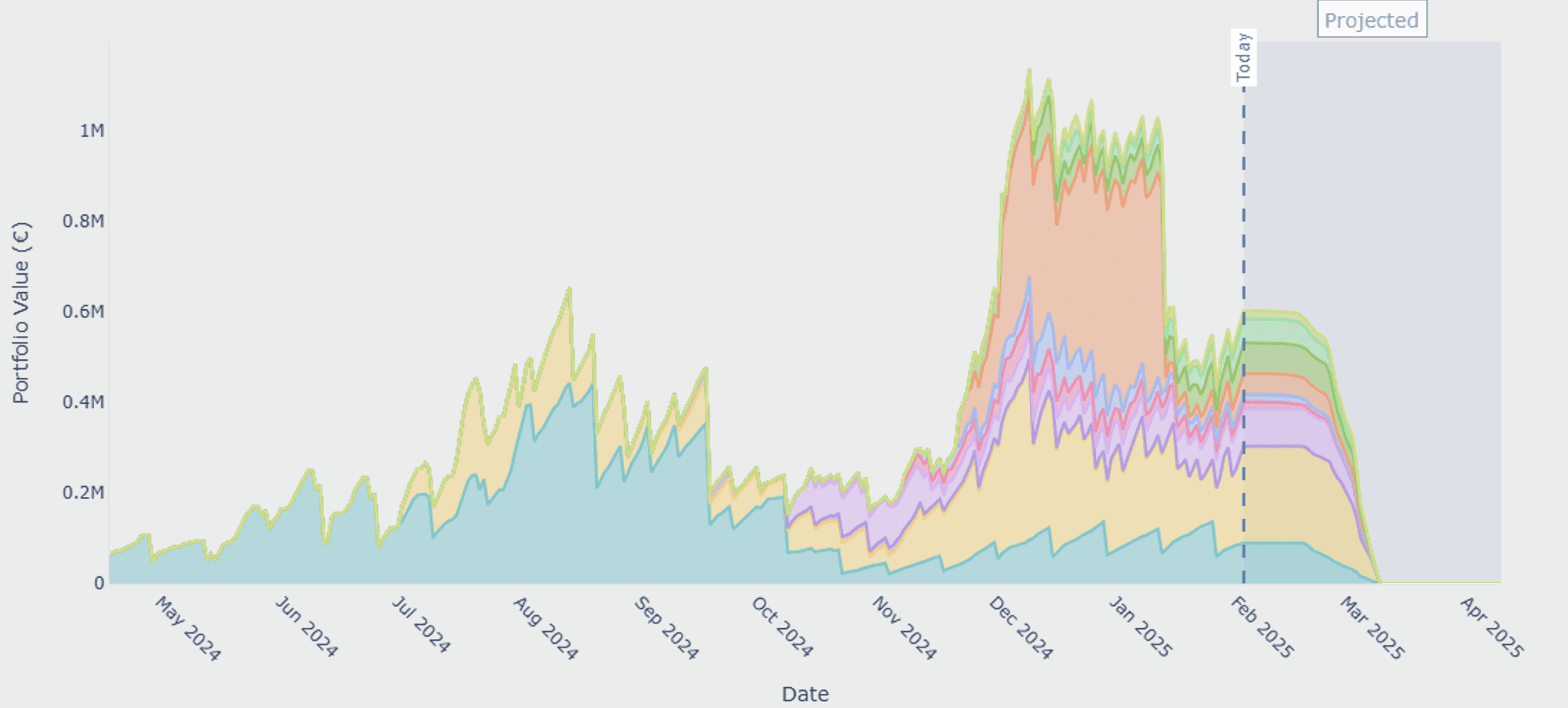

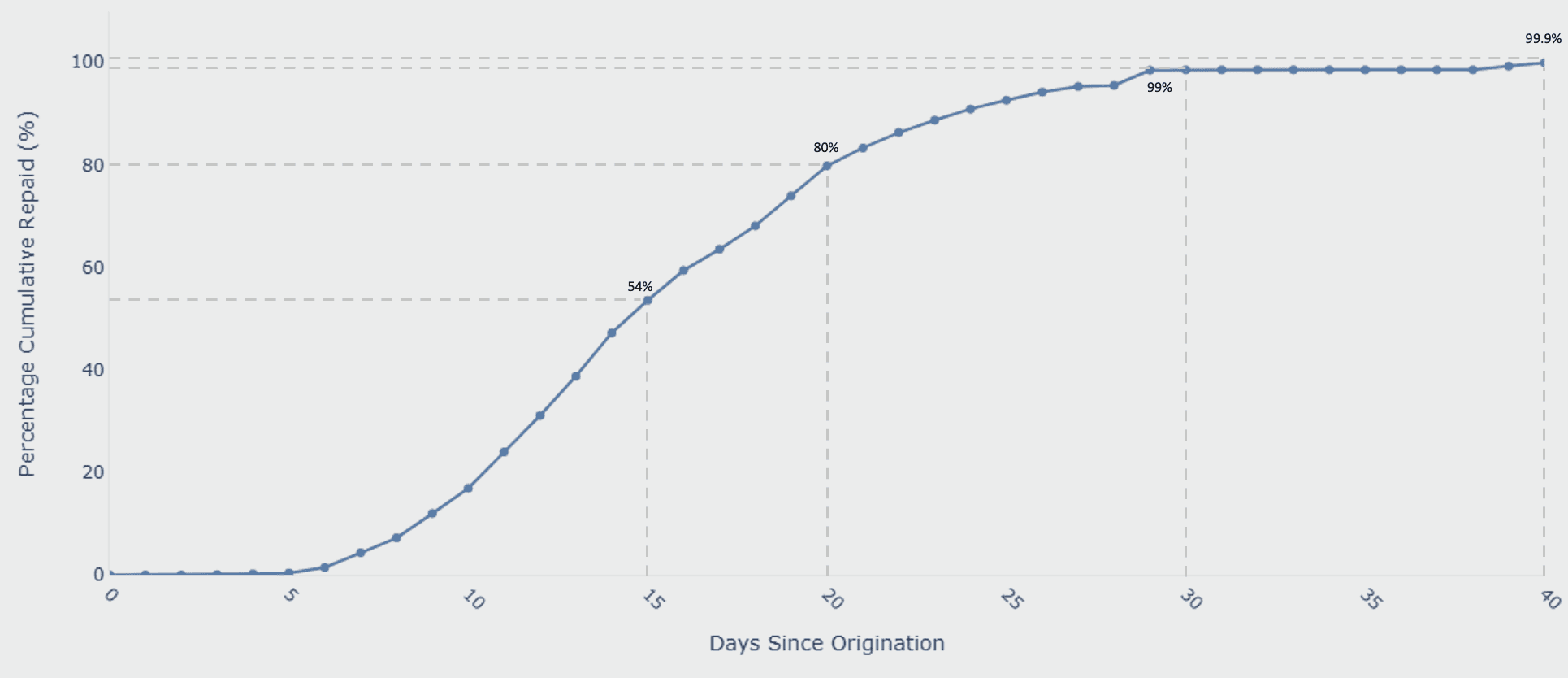

With business intelligence and predictive analytics, fintechs gain visibility and transparency into their performance, reducing manual workload while supporting proactive, data-driven decision-making. These insights can also help teams adjust underwriting criteria, optimize pricing, and refine collections strategies before issues arise. Delivering investor-grade analytics also makes a fintech appear professional and institution-ready, boosting credibility with capital providers and potentially securing better terms. Fence embeds these capabilities directly into operational data flows and offers tools such as the pre-deal tool, which structures loan tapes and highlights asset performance before a facility closes. Below you can see sample outputs: a portfolio value chart showing client evolution over time, and repayment curves illustrating how quickly loans are repaid.

Outstanding portfolio breakdown with historical performance and projected forward values.

Cumulative repayment curve of assets, showing that 99.9% of loans are repaid within 40 days of origination.

Alerts

Staying on top of every detail is critical for lean fintech teams. Fence’s automated alerts flag delayed payments, covenant breaches, or threshold violations in real time, ensuring that issues are addressed before they escalate. This helps fintechs meet compliance requirements, avoid costly oversights, and reduce monitoring overhead, all while giving fintech teams peace of mind, reducing fire drills, and helping them operate like a trusted organization. For early-stage fintechs, scaling with institutional capital requires more than growth—it demands trust, discipline, and transparency. With solid lending workflows, asset-based financing infrastructure, and advanced monitoring, originators can evolve from managing loans to building a scalable, institution-ready platform that fuels sustainable growth.

Finally, beyond technology, Fence has also built a network of fintech lenders and capital providers. We help connect fintechs to the right capital partners based on their criteria and financing needs, making it easier to find the best fit for their next facility. To join the network, simply fill out this short survey.

Fence supports this journey from end to end, helping fintechs grow faster while meeting market standards. Whether you’re starting out or preparing for your first debt facility, we’re here to guide you. Excited to connect!